MINDFORGE INTELLIGENCE

Market Risk Classifier

THE DATA BUYER

BRIEF

[ Orthogonal Regime Data — Inputs, Outputs, Evaluation ]

SYSTEM CONTEXT

Market Risk Classifier (MRC) : Daily regime classification. Delivered pre-market. Research tool, not trading signal.

INPUT CLASS : Space weather telemetry from NOAA and NASA — the same input class Federal Reserve research (Krivelyova & Robotti, 2003) tied to equity returns.

CORE FINDING

A daily regime feed nobody else has.

Orthogonal to VIX, options flow, sentiment, and macro.

Backtest: 2012–2024 • 92.31% precision (CRISIS, 12/13, backtest) • 2025–2026 out-of-sample • mindforge.tech/terms

INPUTSWHAT THE DATA ISInputs, Processing, Output, Delivery

INPUTS

Space weather telemetry from NOAA and NASA monitoring networks — the same input class Federal Reserve research (Krivelyova & Robotti, 2003, FRB Atlanta WP 2003-5b) tied to equity returns.

ORTHOGONALITY

Structurally uncorrelated to VIX, options flow, sentiment, and macro indicators — a genuinely independent axis of information.

PROCESSING

Rules-based, not ML. Fixed thresholds with rolling 252-day normalization. Walk-forward only.

AUDITABILITY

Versioned rules with full audit trail. No model drift, no retraining, no hindsight tuning.

OUTPUT

5 daily regime states: STABLE, SHIFTING, ELEVATED, SHOCK, CRISIS. Single classification per day. No intraday noise.

HISTORY

5+ years of historical classifications included for evaluation. Extended history (35 years) available under pilot agreement.

DELIVERY

Delivered pre-market every trading day.

CHANNELS

API (REST, JSON) · Email (rich HTML) · CSV (S3, SFTP) · Webhook on state change (<5 min latency)

Cross-era CRISIS 1990–2011 backtest history available at mindforge.tech/market-risk-classifier/systemic-stress-history.

STATESTHE 5 REGIME STATES2012–2024 backtest • 2025–2026 out-of-sample

| State | What it classifies | Precision | Hits/Total | Freq/Yr |

|---|

| CRISIS | Crisis-level regime: COVID, carry unwind, tariff shock | 92.31% | 12/13 | 0.4 |

| SHOCK | VIX expansion without systemic collapse | 85.07% | 57/67 | 1.9 |

| SHIFTING | Regime pivot point: transition between states | 92.75% | 64/69 | 2.0 |

| ELEVATED | Elevated conditions, advisory-level warning | 75.51% | 37/49 | 1.4 |

| STABLE | Benign regime: reduced risk posture appropriate | Meta | — | ~87% of days |

WHY 5 STATES, NOT RISK-ON / RISK-OFF

The system distinguishes a SHOCK (VIX expansion) from CRISIS (crisis-level). Oct 2024 was SHOCK, not CRISIS — no forced liquidation on a temporary expansion. A binary toggle would have over-reacted; the granularity is what makes the feed usable daily.

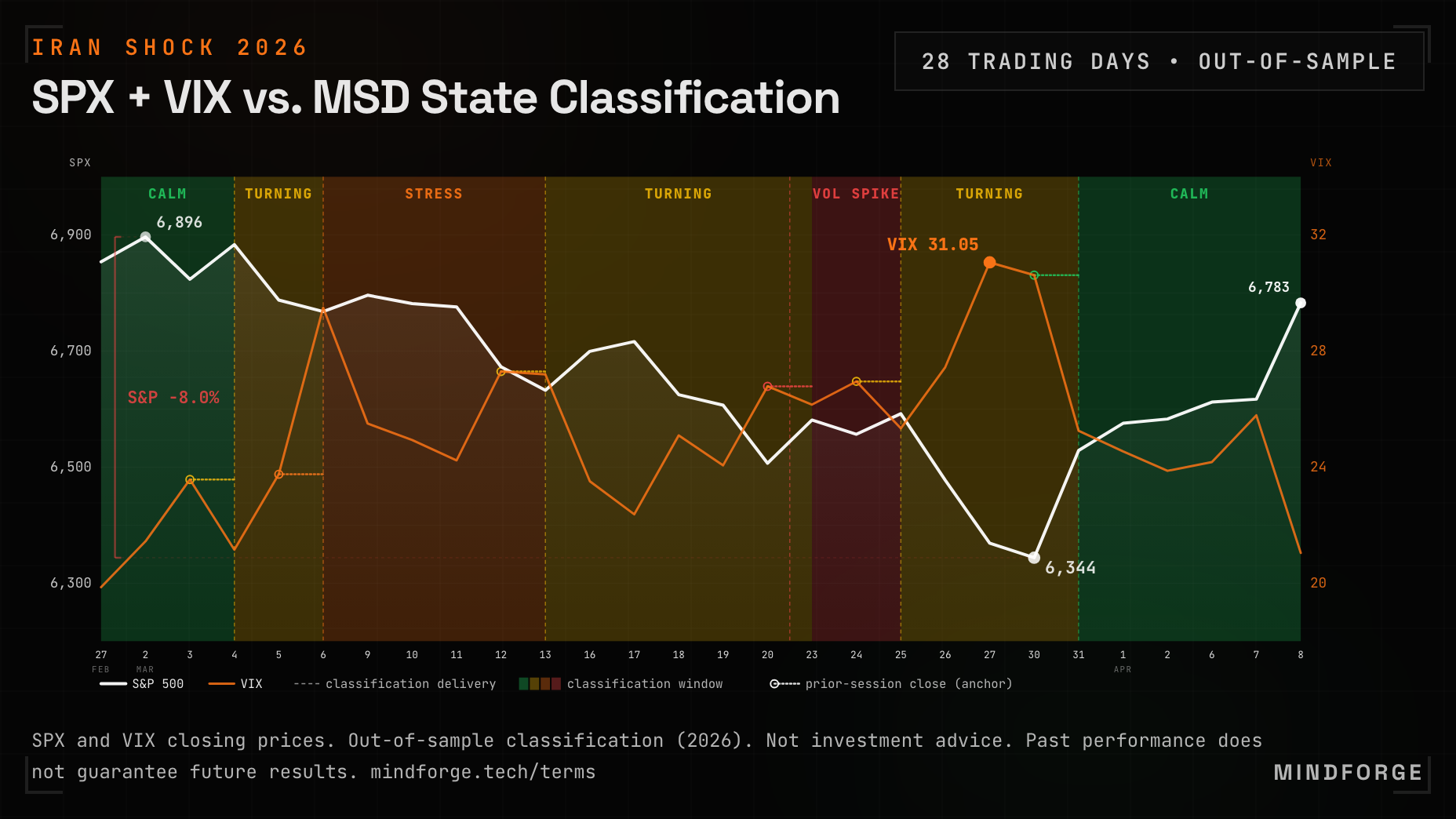

PROOFLIVE PROOF — IRAN SHOCKMar 2026 • production classifications • not backtested

THE TAPE

STABLE (Feb 27) → SHIFTING (Mar 4) → ELEVATED (Mar 6) → SHIFTING (Mar 13) → SHOCK (Mar 21, eff. Mar 23) → SHIFTING (Mar 25) → RESOLVED (Mar 31). Six transitions, 28 trading days.

CLASSIFIED PRE-MARKET

Every transition delivered before the trading session opened, by 07:30 ET — production classifications, not back-stamped.

PEAK & TROUGH

VIX peaked 31.05 (Mar 27, CBOE close); S&P trough 6,344 (Mar 30). Same deterministic rules validated on 2012–2024 — no overrides.

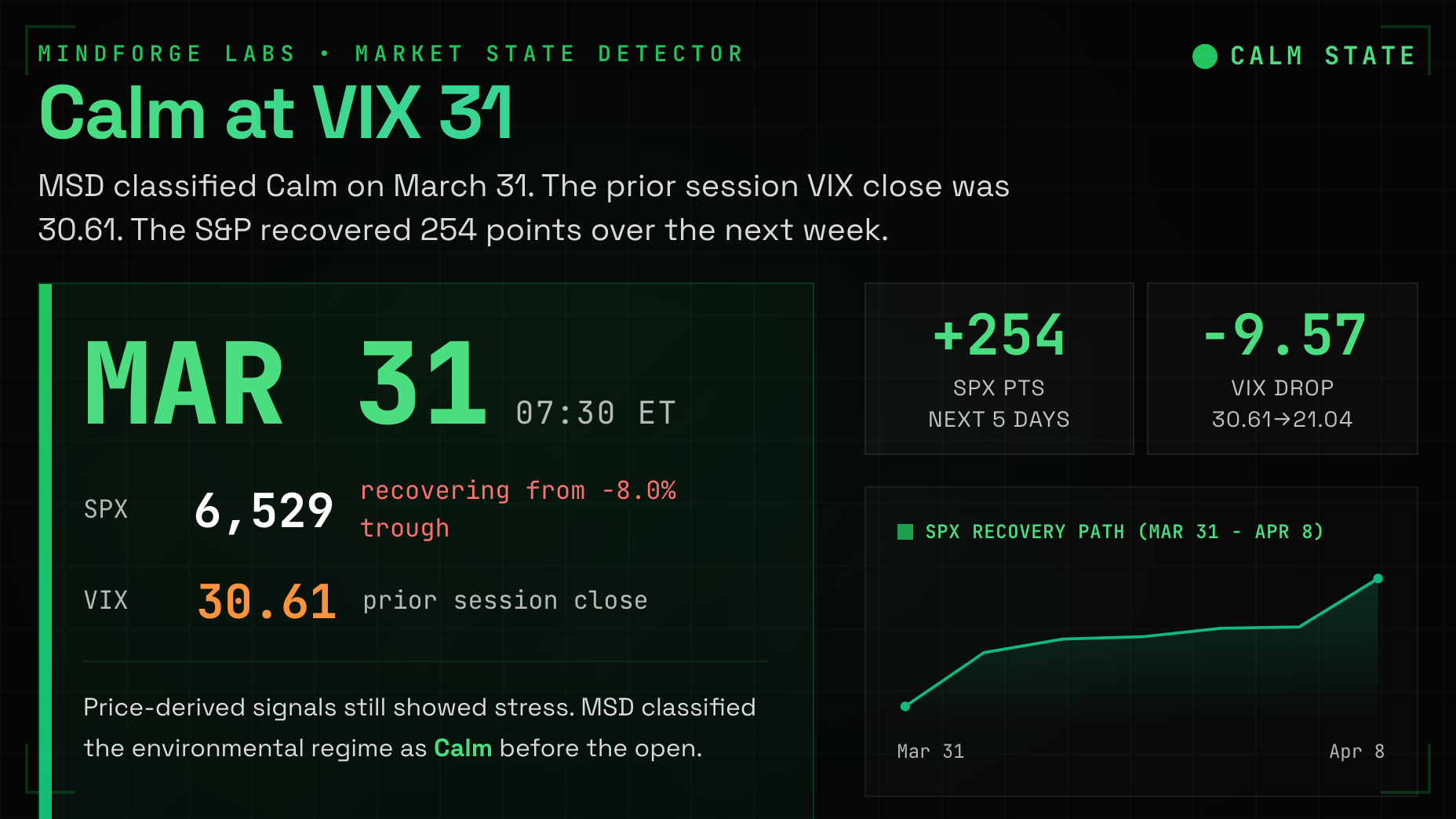

PROOFRESOLVED AT VIX 31Mar 31 2026 • the orthogonality moment

THE CALL

On Mar 31 MRC classified RESOLVED with the prior-session VIX close at 30.61 — while headlines still ran crisis narratives and price-derived signals said stay defensive.

WHY IT IS POSSIBLE

MRC’s primary inputs are environmental, on timescales independent of price. When those inputs normalized, the system said so — regardless of where VIX sat.

WHAT FOLLOWED

By Apr 8, VIX was back near 21 and the S&P had recovered +254 points. A VIX-reading signal cannot call normalization while VIX is still elevated — by the time it confirms, the move is behind you.

EVALUATIONPRIOR EPISODES & INTEGRATIONFrom canonical records • 60-day pilot terms

10

Trading Days Early

COVID-19 • SS 2020-02-24

Before first s&p 500 circuit breaker

1

Trading Day Early

Carry unwind • SS 2024-08-02

Before flash crash / vix spike to 66

22

Trading Days Early

Tariff episode • VS 2025-03-06

Before tariff-driven vix peak

60-DAY PILOT

Full production feed. 60-day license.

BACKTEST

5+ years historical classifications (extended history under pilot).

SCORING

Pre-defined success criteria.

COMMITMENT

No commitment beyond pilot.

API

REST/JSON, historical + live endpoints.

EMAIL

Rich HTML, daily pre-market.

CSV

Daily drop (S3, SFTP, email).

WEBHOOK

State-change push (<5 min latency).

AUDIT TRAIL

Versioned rules with integrity verification.

EPISODES

Episode catalog with exact dates and values.

METHODS

Walk-forward methodology documentation.

COMPLIANCE

Research-only framing, no advice language.

SAMPLE OUTPUT (API RESPONSE)

{

"date": "2026-03-21",

"state": "volatility_spike",

"previous_state": "turning",

"delivered_at": "2026-03-21T07:28:00-05:00",

"rule_version": "2.0.0"

}ACCESSPILOT

VERIFY IT LIVE

60 Days. Full Access.

INCLUDES

- • Full production feed for 60 days

- • 5+ years historical classifications

- • Pre-defined scoring & success criteria

- • Due diligence documentation package

QUALIFICATION

Institutional 60-day pilot for qualified research teams.

RESTRICTED TO INSTITUTIONAL USE